Driving through Malaysia’s scenic roads comes with responsibilities, and having the right motor insurance coverage is a key part of that journey. Whether you’re a seasoned driver or new to the roads, understanding the different types of motor insurance available, ensuring a worry-free drive across the stunning landscapes of Malaysia.

In this guide, we’ll explore three main types of coverage that form the backbone of car insurance in Malaysia, delve into the realm of optional coverage and some of the factors that affect your insurance premium.

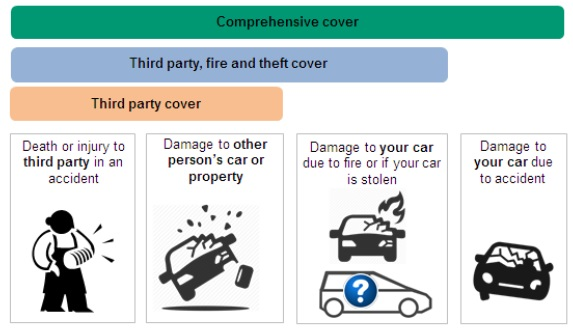

The Types of Motor Insurance Coverage in Malaysia

1. Third-Party Coverage: Looking Out for Others

Picture this: you accidentally bump into another car while parking. That’s where Third-Party Insurance steps in – it covers the damages caused to someone else’s car or property. However, keep in mind, it won’t fix your own car or cover any injuries you or your passengers sustain.

Who benefits:

This type of insurance is ideal for those driving older cars with lower market value, where comprehensive coverage might be too expensive. Additionally, if you’re on a tight budget or driving infrequently, third-party insurance can be a practical choice.

How it works:

Suppose you’re involved in an accident where you’re at fault. Your insurance provider will cover the expenses for the other party’s injuries or property damage, excluding the repair costs for your vehicle.

2. Third-Party, Fire, and Theft Coverage: Shielding Against the Unexpected

Imagine waking up to find your car missing. Third-Party, Fire, and Theft Insurance (TPFT) come to the rescue by covering damages due to fire, theft, or if your car decides to grow wings and disappear. But remember, it’s not as extensive as comprehensive coverage.

Who benefits:

Suited for savvy budgeters and owners of mid-value cars, TPFT offers a sweet spot, providing more coverage than basic insurance without the hefty price tag of comprehensive plans. It’s a gem for urban explorers in theft-prone areas, acting as a vigilant shield against theft or attempted theft.

How it works:

In action, TPFT acts as your reliable co-pilot—covering damages or injuries to others in accidents where you’re at fault, safeguarding against fire damage, and offering support in case of theft or attempted theft. However, keep in mind, when it’s your fault in an accident, TPFT won’t cover your car’s repair costs, but it’s that perfect middle ground ensuring a worry-free drive without burning a hole in your pocket.

3. Comprehensive Coverage: Your All-in-One Shield

Want more protection? Say hello to Comprehensive Insurance! It’s like a superhero cape for your car, covering not only third-party liabilities but also theft, fire, accidents, and even acts of nature like floods or earthquakes. Plus, it might chip in for medical expenses and personal accidents too!

Who benefits:

Comprehensive coverage is suitable for owners of newer or higher-value cars, as it offers complete protection for your vehicle against various risks. Additionally, frequent travelers or those residing in theft-prone areas might find this coverage beneficial.

How it works:

In the event of an accident or theft, comprehensive insurance covers repairs or replacements for your vehicle. Moreover, it can extend to cover personal accident benefits for the driver and passengers.

Refer below infographic to help you better compare each coverage to choose the right insurance:

Infographic source: Persatuan Insurans Am Malaysia (PIAM)

Additional Coverage, Extra Layers of Protection You May Need

1. Windscreen Protection: Keeping Your Journey Smooth

A sudden crack or chip in your windshield could put a dent in your day, quite literally. But with windscreen protection, those worries vanish. This coverage shields you from the costs of repairing or replacing a damaged windscreen, keeping your journey smooth and stress-free. It’s a game-changer, especially on Malaysia’s bustling roads where surprises can pop up anytime. Don’t let a cracked windshield crack your day – opt for windscreen protection and keep your travels carefree!

2. Special Perils Coverage: Nature-Proofing Your Ride

Malaysia’s weather can be unpredictable, right? Special Perils Coverage extends beyond the usual and protects your vehicle from nature’s tantrums like floods, landslides, or hurricanes. It’s like giving your car an umbrella for any weather!

3. Additional Drivers: Avoiding Penalties and Costs

Picture this: a mishap on the road involving someone else driving your car might lead to a hefty RM400 penalty in Malaysia, known as the unnamed driver excess. But fear not! Adding extra drivers to your car insurance could save the day. By including additional drivers on your policy, you dodge this penalty if they’re in an accident while driving your car. Bonus: most Malaysian insurers offer the first additional driver inclusion at no extra cost!

Now, here’s the catch: beyond that first freebie, each added driver usually incurs a RM10 fee, tacked onto your insurance premium. Insurance typically covers up to five drivers, including yourself. So, say you add four extra drivers—that’ll be an extra RM30 to cover them all.

4. Legal Liability to and of Passengers: Your Safety Net on Malaysian Roads

Covering both sides of the passenger coin, legal liability coverages ensure peace of mind on Malaysia’s roads. First up, Legal Liability to a Passenger (LLTP) safeguards you from legal hassles if your passengers file claims due to an accident where you’re at fault. This coverage handles any liabilities toward your passengers, be it injury or damage to their belongings, typically priced at about 25 percent of a basic third-party insurance policy. On the other hand, Legal Liability of a Passenger (LLOP) steps in when someone outside your vehicle claims against you for your passengers’ actions, like if they accidentally harm a pedestrian. Surprisingly affordable at just RM7.50 per annum, LLOP offers tranquility at a budget-friendly rate compared to LLTP.

5. Coverage for Accessories and Modifications: Protect Your Style

Coverage for accessories and modifications acts as a safety net for your personalized upgrades—think snazzy rims or premium audio systems. Here’s the deal: you can get these add-ons insured with a convenient add-on coverage, usually priced at around 15 percent of your accessories’ value. For instance, if your modifications total RM10,000, the add-on cost would be RM1,500. This coverage shields your unique enhancements from unexpected damage or theft, letting you hit the road with confidence, knowing your personalized ride is fully covered!

6. Waiver of Betterment: Unlocking Savings

This nifty addition saves you from shelling out extra cash when repairing an older car after an accident. Essentially, it covers the cost difference between old and new car parts during repairs, ensuring you’re not stuck footing the bill for upgrading your car’s components. With the Waiver of Betterment in your insurance arsenal, maintaining your trusted ride becomes much easier and lighter on the wallet!

7. e-Hailing Insurance: Safeguarding Your Ride-Hailing Venture

Looking to safeguard your hustle as an e-hailing driver in Malaysia? E-hailing insurance is your golden ticket! Specifically designed to cover drivers transporting passengers for hire, this insurance provides the protection you need when you’re on the road, ferrying passengers from point A to B. Not only does it meet legal requirements, but it also shields you and your passengers in case of unexpected twists on the journey. Whether you’re driving for Grab, MyCar, or any other e-hailing service, having this coverage is crucial. It ensures that your ride-hailing venture is backed by the safety net of comprehensive insurance, letting you focus on delivering a smooth and secure ride every time.

Factors Affecting Your Insurance Journey

Now, let’s talk about what might steer your insurance costs:

a. Your Ride’s Make and Model

Fancy cars might mean higher premiums due to higher repair costs. So, that sleek ride of yours might demand a bit more from your pocket.

b. Car Market Value

A car’s market value diminishes every year, and this decline directly influences insurance premiums. Generally, vehicles with higher market values incur pricier insurance premiums.

c. Driver’s Profile Comes into Play

Your age, driving history, and experience are road signs for insurers. Young or inexperienced drivers might pay more due to perceived higher risk.

d. Purpose of Your Drive

Is it for personal joyrides or work? Commercial vehicles might ask for higher premiums due to more exposure on the roads.

Tips for Your Insurance Trip:

- Know Your Car’s Worth: Match the coverage to your car’s value—it’s key!

- Compare Quotes: Shop around for deals that match your budget.

- Add-Ons Matter: Choose extras like windscreen protection or accessory coverage that suit your needs.

- Check Reviews: Peek at reviews to find an insurer that’s reliable and trustworthy.

- Understand Coverage: Don’t overlook the fine print—know what you’re getting!

Wrapping Up Your Insurance Adventure:

With diverse coverage options available in Malaysia, finding the right insurance is like choosing the perfect travel buddy for your road trip. So, before hitting the road, assess your needs, compare policies, and understand the terms and conditions. Remember, insurance is your safety net, but responsible driving is your steering wheel to a safer journey for you and everyone else on the road.